Is the economy going like gangbusters or about to fall apart?

I have mentioned before that I think we are headed for a deep recession. The warning signs are there and in a year or so, everyone will look back and say, "we should have seen this coming!" In the post-pandemic era, we've seen people start to spend money again, much as they did after World War II. And just like the late 1940's, there are shortages of everyday commodities, cars, and people. Folks are going out on strike, all over the place, because wages are not keeping up with inflation.

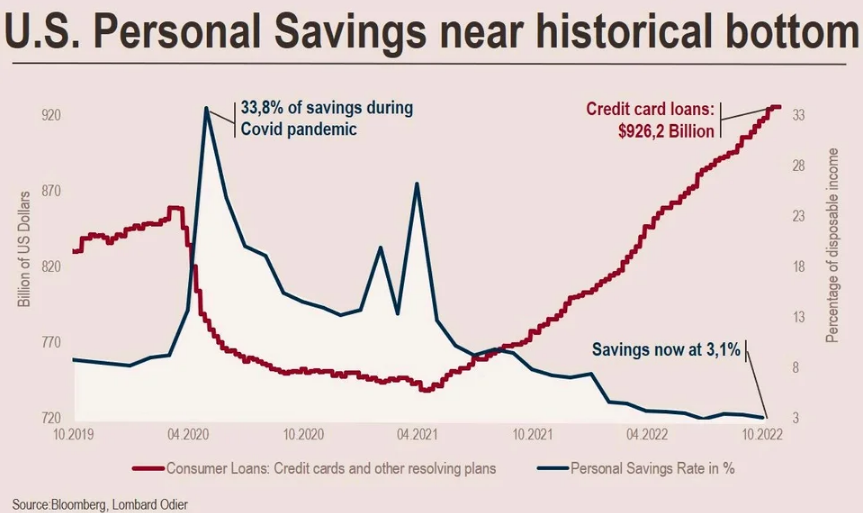

The chart above, which can also be found in interactive form, online, illustrates what is happening to the average American in coping with this inflationary trend. People have not yet cut back on spending, or even speeding - they just whine and complain about gas prices. It takes a while for people's habits to change, and cutting back is far, far harder than expanding your budget - something I learned back in 2011 when I started this blog.

So it is human nature that we grouse about prices - but keep buying anyway. We dip into savings and borrow more on credit cards and think, "this too, shall pass!" and somehow later on, we'll catch up and pay off that credit card and restore the balance in our savings account. That never happens, of course. What happens is that we wake up some day and realize the balance on our accounts are low - maybe the wake-up call was a bounce notice. And maybe another wake-up call is the fact we are barely making the minimum payments on our credit cards. It seems to happen suddenly, even though the process has been in the making for months, if not years.

So we try to cut back. Gee, maybe not driving 80MPH might save some gas! Maybe we should plan our trips, so we aren't driving back and forth to town, three times a day! Maybe we don't need to look at "shopping" as a hobby. Maybe it is time to take back some things we bought months ago, that were never even unpacked, and get a refund! Maybe we need to shop at Walmart instead of Wegmans! Maybe we need to have a garage sale! Maybe it is time the hobby car or boat or motorcycle goes away!

Maybe. I've seen it before. I've lived it. And it wasn't all that bad. Expensive habits are easy to accumulate, hard to shed. But once you shed them, you look back and think, "I used to go to the coffee shop nearly every day and drop $5 to $10 on coffee! Was I nuts or what?" Because once you think about money and what it means, well, you stop being careless with it. It is your life, your freedom.

And I can already anticipate the negative response to that last statement. "There is more to life than money, man!" says the 30-something who has intractable credit card debt, "Money can't buy happiness!" Yes, of course, but lack of money can buy all the misery you can stand.

You don't have to worship money, you just have to respect it, and spending your wealth willy-nilly isn't being respectful to yourself. I noted early on in this blog that a credit card is like a loaded handgun - a useful tool, perhaps, in some situations. But used carelessly, it can cause tragedy.

I mentioned before that we are due for a housing crash, or at the very least, an "adjustment." Prices that made sense with a 3% mortgage make a lot less sense at 7%. You can't just expect people to increase their mortgage payments by half - the money has to come from somewhere. When it is cheaper to rent than to buy, why buy? And when housing prices drop, it will make consumers even more nervous about spending. The snowball effect kicks in, yet again.

"But Bob!" you say, "Housing prices are still going up! Companies are making record profits! Unemployment is way down! Things are going great!" And maybe that is true. Or maybe there is a lot of hysteresis in the system. I recounted before that back in 2005 or so, we bailed on the housing market. We sold our condos in Florida, our duplex in Alexandria, and our office building in Old Town and even our house. We made a lot of money, and the people we sold to, well, some of them went into foreclosure. Today, those properties are worth more than we sold them fore - a lot more - but there was a decade there where things were upside-down.

How did I know when to sell? Simple. Most of those properties were bought after the housing market crash of 1989. And all the signs of the crash of '89 were present, even moreso, in 2005. I thought for sure the market would collapse in 2006 or so. It kept going another two years. Timing this shit is hard to do. It takes a while for people to come to their senses. Markets are not efficient.

For example, I failed to consider that, after the pandemic was "over" (such as it is) that people would come out of hiding and there would be a lot of pent-up demand. So sales went crazy, as the above chart illustrates. People saved up a lot of money during the pandemic, mostly because they weren't commuting, I am guessing, and once things reopened, people spent that money, which fueled inflation.

But be that as it may, there are hard lines here that can't be crossed. How folks can afford houses today, with interest rates more than double that of a year ago - and at higher prices to boot! - is beyond me. The last two times around - 1989 and 2008 - we saw a lot of people "panic buying" toward the end. Real Estate Agents told them, "buy now before you are priced out of the market forever! Bu-wha-ha-ha!" And the folks who were patiently biding their time, thinking that prices couldn't go up much further, panicked and bought at the peak - and lost it all within a year or so.

Could it happen again? Something has to give, I think. But then again, predicting the future isn't an easy task. Maybe the "labor shortage" will cause wages to rise and people can then afford these crazy prices and pay off their credit cards. I doubt it though. Having lived through a "stagflation" period, I know how that works. Wages go up, which drives prices up, and you end up swimming in place.

We'll just have to wait and see. Timing markets is not an easy job.

UPDATE: A reader notes this recent Wall Street Journal article, which I noticed after writing this piece. The WSJ, a Murdoch publication (a disclaimer you should put after referring to any Murdoch publication) believes that people have tons of money from the pandemic, all because of those $1200 stimulus checks.

I think either they are thinking of their readers, whose average income and savings indeed is far above the average, or their information is dated. Indeed, we see people from Atlanta snapping up houses here on our island, paying record prices, often in cash. But maybe the WSJ is looking backward at outdated data. Eventually, the spending orgy has to end.

The stock market, particularly tech stocks, are getting hit, which decreases "savings." And with inflation, people have to spend more and save less - and borrow more as a result.

I know that personally, we have increased our spending by about $5,000 a year, just to keep up with inflation. This, in turn, has decreased our savings by the same amount. We are hardly at the point of going broke.

But I suspect some are....